A Gateway of Finance: The Development of the Kansas City Federal Reserve, 1914-1935

In the second decade of the 20th century, Kansas City was emerging as a key center of economic power west of the Mississippi. Agriculture constituted a central pillar of Kansas City's success: dozens of railroads shipped grains and livestock through the city’s new hub at Union Station, and its manufacturing district developed large meatpacking, flour, and other food processing industries. Wholesale and retail commerce joined agriculture and industry as the foundations of Kansas City’s economic power.

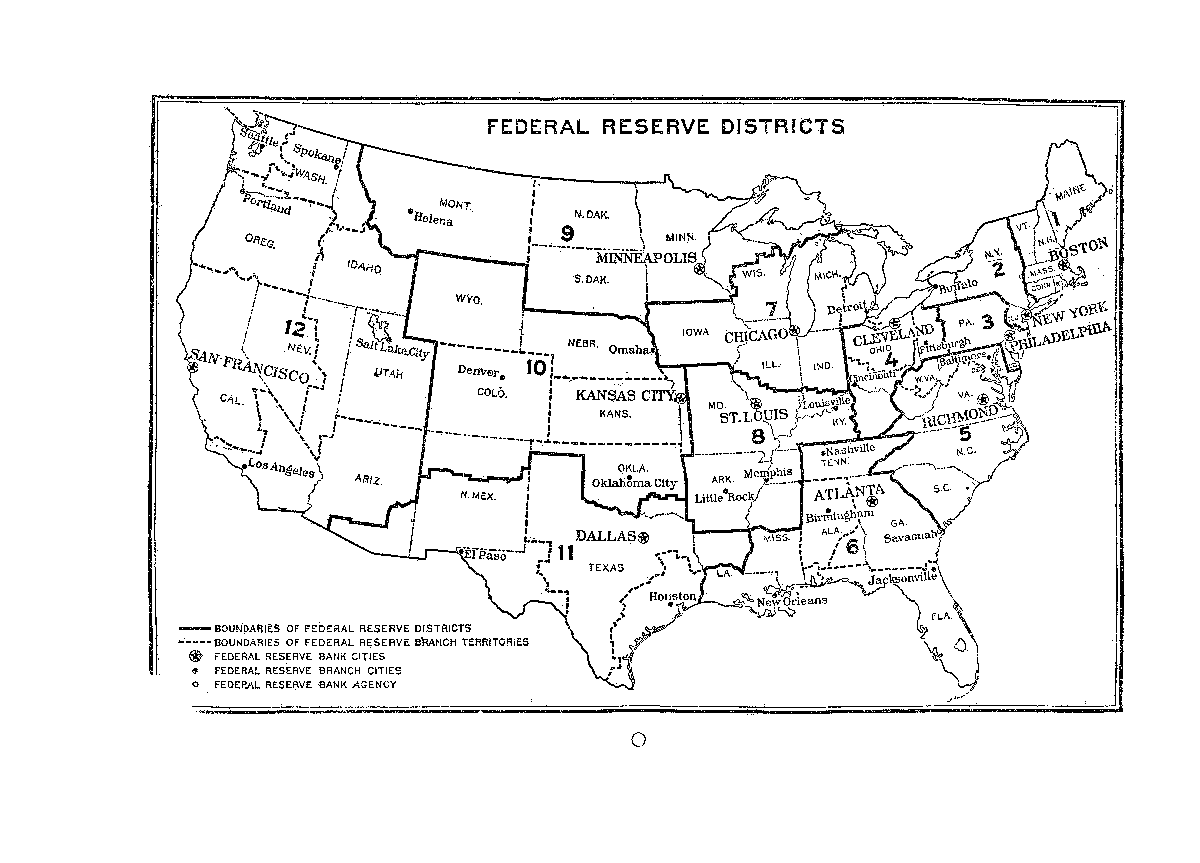

Kansas City’s status as a commercial center in the West made it a contender for a regional branch of the Federal Reserve System, established by the U.S. Congress with the Glass-Owen Bill on December 23, 1913. The movement to include Kansas City among the list of 12 regional hosts for Federal Reserve Banks demonstrated its economic strength as a western “gateway city,” second only to Chicago and equal to St. Louis and Minneapolis.

The location of a Federal Reserve branch in Kansas City also represented the increasing political power of a western region unhappy with the nation’s current financial structure. Lacking a central banking system since President Andrew Jackson rejected the charter of the Second Bank of the United States in 1836, the United States had developed a mixed system of state and national banks with diverse regulations and few policy controls. Funds from smaller banks tended to flow eastward in the form of investments in the New York Stock Exchange, and the whole economy had a propensity to dissolve into crisis when the stock market stuttered. Lawmakers had witnessed this most recently in the Panic of 1907. The designers of a system of 12 regional banks, located in smaller cities such as Minneapolis and Kansas City, as well as in the large financial centers of New York and Chicago, intended to disperse the power of the nation’s elite bankers.

The Federal Reserve was an instrument for challenging the nation’s traditional economic hierarchy, and Kansas City played an important role in efforts to balance the economic power of the nation’s interior and western regions with that of the eastern seaboard. The Federal Reserve Bank of Kansas City was supposed to provide a more secure and equitable system of distributing credit for agricultural, industrial, and commercial development throughout its region. Encouraging member banks to provide adequate credit to the Great Plains—a region economic elites had dismissed as the "hinterlands"—would allow it to flourish under its own financial power. Proponents of the Kansas City Federal Reserve Bank hoped that the city would wield substantial power in lifting its region to new economic heights.

In its first two decades, however, the Federal Reserve struggled to stabilize the regional agricultural economy. Its policy of raising interest rates to slow down the post-World War I economy depressed the prices of agricultural commodities and alienated residents of the broader region, while doing nothing to stop banks from sending their funds to Wall Street. As the economic consequences spread to other industries and the Great Depression began, unstable banks closed by the thousands. The Federal Reserve Bank did not yet have the precedent for strong policy intervention, and so during these years it was unable to capitalize upon Kansas City’s commercial position and boost the regional economy out of the doldrums.

City leaders came together with businessmen from throughout the proposed Federal Reserve district to promote Kansas City’s bid for the regional bank. William Rockhill Nelson, publisher of the Kansas City Star, touted the “West Bottoms which receives a steady stream of cattle from the whole West up to the Rocky Mountains,” the “immense industrial development that is going on in North Kansas City,” and the “New Union Station,” which symbolized the railroads’ commitment to shipping the region’s goods through Kansas City.

The Commerce Trust Company, presided over by William T. Kemper, as president, issued a letter in support of the city's bid. Kemper was among the dignitaries present to speak for the city and region at the January 23, 1914, Organization Committee hearing. The vice president of Commerce, Jo Zach Miller Jr., would soon serve as the regional governor of the Federal Reserve Bank of Kansas City.

Among Kansas City’s other boosters were associations including the Kansas City Commercial Club, Cooperative Club, Millers’ Club, Motor Car Dealers Association, Life Underwriters’ Association, Live Stock Exchange, Rotary Club, Southwestern Lumbermen’s Association, and the Western Retail Implement, Vehicle, and Hardware Association. R.J. Thresher, president of the Kansas City Board of Trade, made it clear that increased credit operations close at hand would grease the wheels of growing industries:

This is the largest primary winter wheat market in the United States. Last year we handled over seventy million bushels of grain. It is the second largest live stock and packing center. These interests together with various other industries which are rapidly growing demand the best possible banking facilities.

Kansas City would gain a great deal from the establishment of a Federal Reserve Bank there, not least the pride of recognition as a financial and commercial center of the nation.

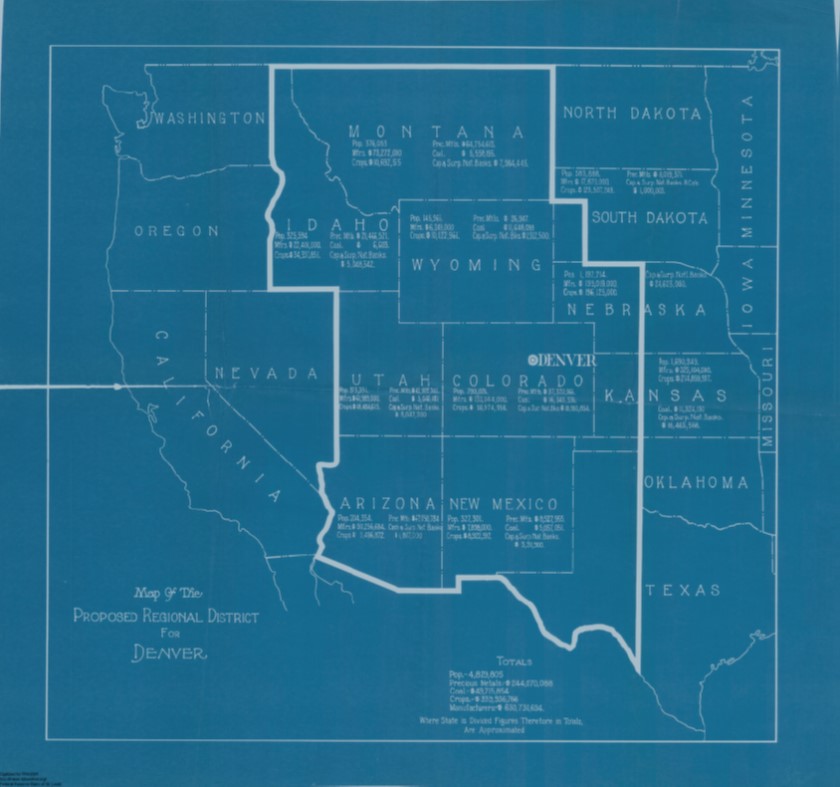

Perhaps even more important than the support from Kansas City for the new Federal Reserve Bank was that of the surrounding region. The testimony of businessmen from the proposed new region proved crucial for securing the regional center in Kansas City as opposed to possible alternatives like Denver, Colorado.

Coloradans even spoke up for Kansas City over their own capital. J.M. Williams of the Citizens State Bank of Lamar, Colorado, wrote to a colleague, "We, of Eastern Colorado and Northern New Mexico, look to Kansas City as our financial center, which supplies us with practically all the money used in our great sheep and cattle business, which is the greatest business we have in this territory.” Williams noted that livestock naturally moved eastward on railways through the Arkansas River Valley, while funds for the business flowed westward from Kansas City. As an example, the banker cited his bank’s recent financing of 170,000 sheep (nearly a third of the regional business). Out of a total of $680,000 in financing, more than $500,000 “was furnished by Kansas City banks either directly or through commission men."

Parts of New Mexico also expressed a preference for Kansas City over the nearer city of Denver. A banker from Roswell argued, “We feel in this part of the country that Kansas City could serve our needs better than any other city located any place in the country from the fact that we get our mail there about one day quicker than to any other point that we are able to use.” Mail service was important for the banking business, which needed rapid and safe delivery of currency, loan documents, and cleared checks.

Kansas, as the centerpiece of the proposed Kansas City reserve district, overwhelmingly supported the Kansas City plan. John R. Mulvane, a prominent banker from Topeka, noted that his bank did 95 percent of its business with Kansas City banks. Kansas State Bank Commissioner Charles M. Sawyer added that 900 out of 930 state banks in Kansas kept accounts in Kansas City banks. The Federal Reserve Bank would build upon these existing financial relationships.

A few other letters from Kansas bankers summed up the regional arguments in favor of Kansas City. Verne Hostutler, the cashier for the Centerville State Bank in Kansas, concluded that while Denver might seem "from a geographical standpoint, to be the logical location for a bank" west of St. Louis, business concerns suggested otherwise. He argued, "The bank clearings show that Kansas City could serve many times the business interests.” E.G. Boughner, cashier at the First National Bank of Natoma, Kansas, commented, "Kansas City is to be the 'New York City,' the center of business of this great agricultural country in the center of the U.S." And J.C. Hopper, president of the Citizens National Bank of Ness City, Kansas, stated it even more conclusively. He wrote to William Gibbs McAdoo, secretary of the treasury and chairman of the Reserve Bank Organization Committee on January 14, 1914: "The railroads of this western country are focused at Kansas City, and it is the gateway of a great territory, young in development, but with possibilities beyond even the imagination of men."

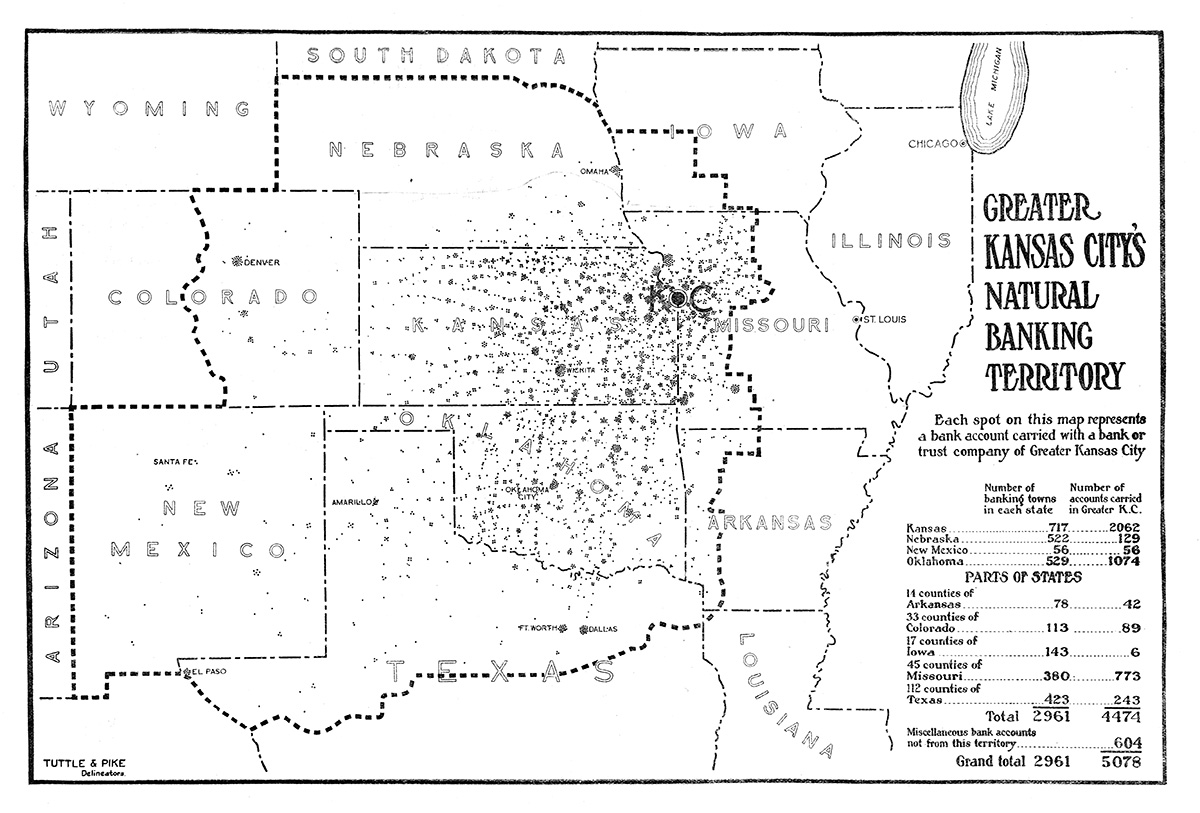

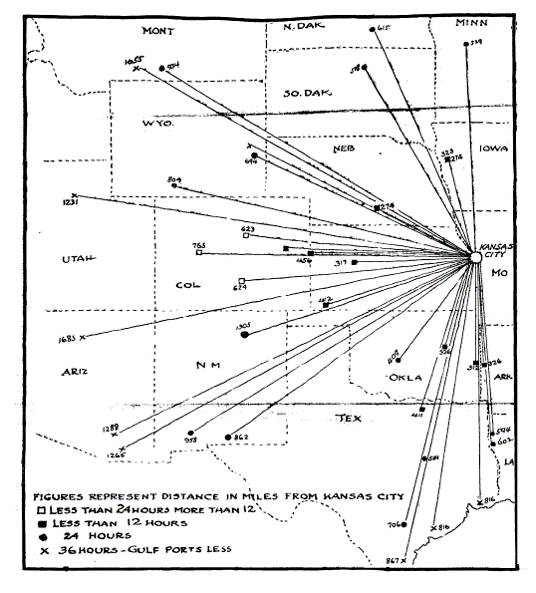

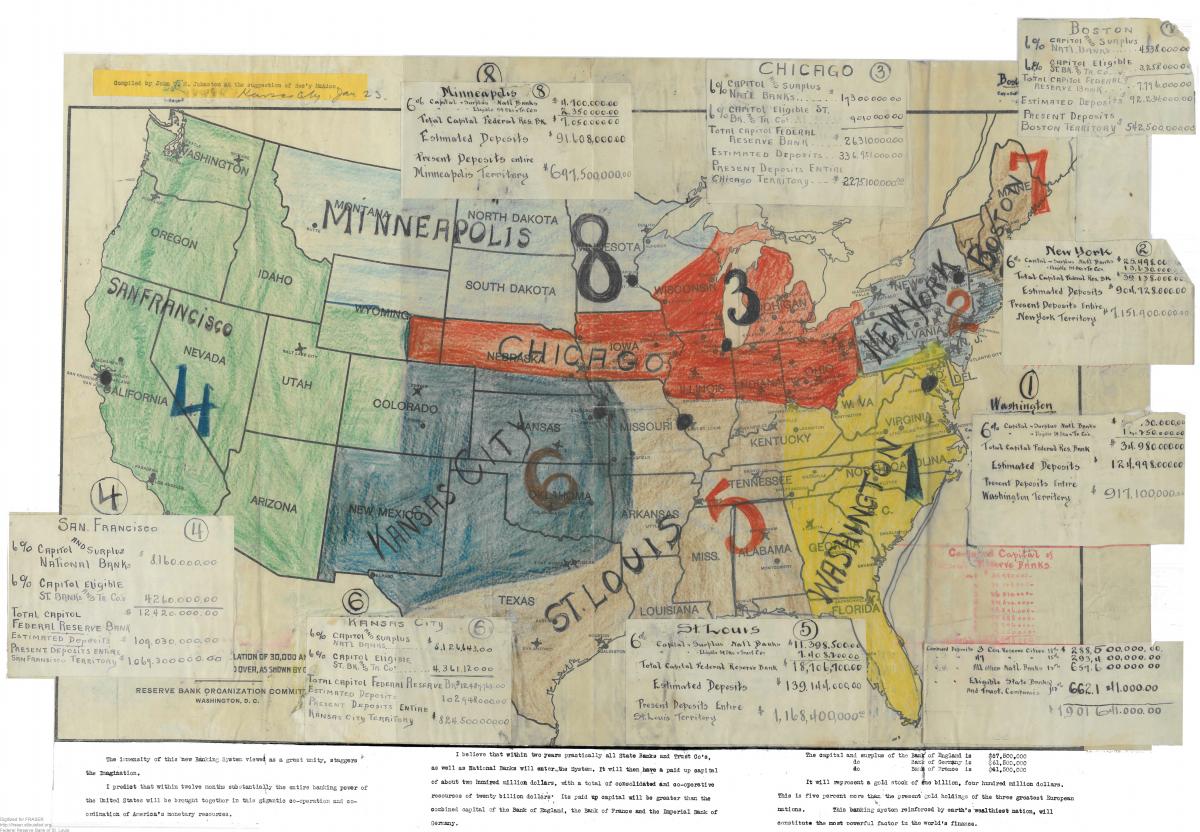

In official testimony for Kansas City’s hearing before the Federal Bank Organization Committee, representatives used several visual aids to supplement this regional support. Maps of money, mail, and commodities flowing into Kansas City underscored its status as a gateway of commerce.

It was clear that designating Kansas City as a Reserve Bank site would build upon the region’s current financial affiliations, contribute to the economic development of the agricultural and natural resource sectors in the region, and shape the industrial and commercial development of the city itself. Kansas City’s selection as one of 12 regional banks proved its coming-of-age as a gateway for financial and commercial interests in the West. While district centers Denver, Omaha, and Oklahoma City would ultimately host branches of the Federal Reserve, Kansas City received the true prize.

Residents of the city expressed pride at its new status. Senator James A. Reed noted before the Commercial Club that whereas few had known of the city before, now it “is recognized by the best authorities as a factor which must be considered in any scheme of business planning.” The Kansas Citian, a journal published by the Commercial Club, demonstrated high hopes for future development as a result of the establishment of the Federal Reserve Bank of Kansas City: “With the richest area capable of unlimited development, of any American city . . . this metropolis must become greater and more extensive . . . . The forecast of the committee that named it for a Reserve Bank will be justified by the outcome.”

The founding of the Federal Reserve Bank of Kansas City had important implications for the conduct of national and regional banking. The flow of funds among all sections of the nation was important both for increasing lending throughout the interior and for times of emergency. During World War I, the Federal Reserve allowed for the transferal of immediate credit among international banks and industries. Because the central bank controlled the nation’s gold supply, bankers did not have to exchange gold physically in this process. The Federal Reserve enabled the conscription of American finances to the democratic cause and helped make the U.S. a financial leader for the world. For many observers, the Fed’s response to World War I demonstrated its ability to navigate perilous economic conditions.

| Year | Items-City Banks | Amount | Items-Country Banks | Amount | Items-Total | Amount |

|---|---|---|---|---|---|---|

| 1919 | 2,002,947 | $3,392,275,705 | 9,173,290 | $2,211,792,134 | 11,176,237 | $5,604,067,839 |

| 1920 | 6,078,269 | $6,320,074,000 | 40,238,898 | $4,227,488,000 | 46,317,167 | $10,547,562,000 |

| 1921 | 6,291,000 | $4,682,326,000 | 43,365,000 | $2,740,027,000 | 49,656,000 | $7,422,353,000 |

| Data compiled by author from Annual Reports of the Federal Reserve Bank of Kansas City, 1919-1935 | ||||||

The Federal Reserve also facilitated several financial services for member banks that paid in capital to the Federal Reserve Bank. It did not transact business directly with the public, but rather served as a “banker’s bank.” It aided regional financial institutions in purchasing their agricultural, commercial, and industrial loans, providing liquid currency to the banks in exchange for holding these assets on its own books. It also served as a clearinghouse for bank checks, provided wire services to expedite the transfer of funds among member banks, and offered educational and professionalization services to bankers across the nation. In its regulatory capacity, the Federal Reserve performed examinations of banks throughout the system and ensured that its members met reserve requirements based on their deposits.

The Federal Reserve Bank of Kansas City performed well through the early 1920s. The bank’s officers identified the institution as “a mighty bulwark of financial strength and National security,” and represented that image in the construction of a large new facility at 925 Grand Avenue. Overcoming initial opposition from prominent Kansas City businessmen Robert A. Long, William T. Kemper, and Jesse Clyde Nichols over the building design, the 300-foot skyscraper became the city’s tallest landmark when it opened on November 16, 1921.

The building’s marriage of traditional stylistic elements with the modernity of skyscraper design and the path-breaking scale of a government-sponsored central banking institution embodied the substantial power the bank hoped to exercise in Kansas City’s financial future. Unfortunately, the bank stood at the brink of two decades of uncertainty, years that would undermine confidence in its powers to mitigate economic downturns.

The first signs of crisis in the region became evident in the agricultural sector during the first few months after World War I. Stock speculation and the prices for consumer goods rose, while farmers in the nation’s midsection faced low prices. The Fed responded to demands for intervention by issuing its first major peacetime policy at the close of 1919. The central bank hoped to stem speculation and inflation by raising interest rates. Regional Fed insiders applauded the interest-raising policy of the next few years, considering it a momentous step in the development of a powerful financial influence.

Ultimately, however, the Fed’s higher interest rates did not impede the flow of money away from the interior and toward the New York Stock Exchange. Though economic conditions in the countryside improved slightly throughout the 1920s, credit levels within Kansas City’s district remained subject to market forces and the whims of bankers who preferred to earn higher profits from investments in stocks and securities. Furthermore, regional observers noted that when lending to local farmers or ranchers, banks simply passed on the Fed’s higher interest rates.

U.S. Senator Robert Owen of Oklahoma, one of the authors of the Federal Reserve Act of 1913, complained that the Federal Reserve’s policy was an “abuse of the powers of the Reserve Banks.” He called for a reduction in the Fed’s interest rate as well as a stronger push to discourage banks “from abusing their trust by sustaining stock speculation.” The senator’s criticisms struck at the heart of the Federal Reserve’s leadership abilities. To Owen and other critics, the Fed’s failure to exercise restraint on its members’ use of borrowed funds indicated its lack of power, or worse, its lack of will to come to the assistance of ordinary Americans.

It was becoming apparent that farmers could not rely on the Federal Reserve to relieve shortages in credit, despite the institution’s stated commitment to agriculture and the related industries that had shaped Kansas City’s development as a powerful trade center. Market forces would determine the availability of agricultural credit, not Fed policy. Consequently, the agricultural sector remained unsteady throughout the 1920s and declined further with the worldwide depression of the 1930s.

Crises in agriculture were meaningful for Kansas City's district and for the city itself, because so much of the regional economy relied on the production of commercial crops and livestock, as well as on the ability to process those commodities into marketable goods. When agricultural markets were weak, as they were through 1922, corresponding industries in the city such as meatpacking and flour milling declined. If commodity prices and agricultural production rose, as they did between 1923 and 1929, industry and commerce in the city recovered. When in 1930, the value of farm products in the district again fell—this time by 31.7 percent—the prices in food processing industries also decreased, followed by lower values of wholesale and retail trade.

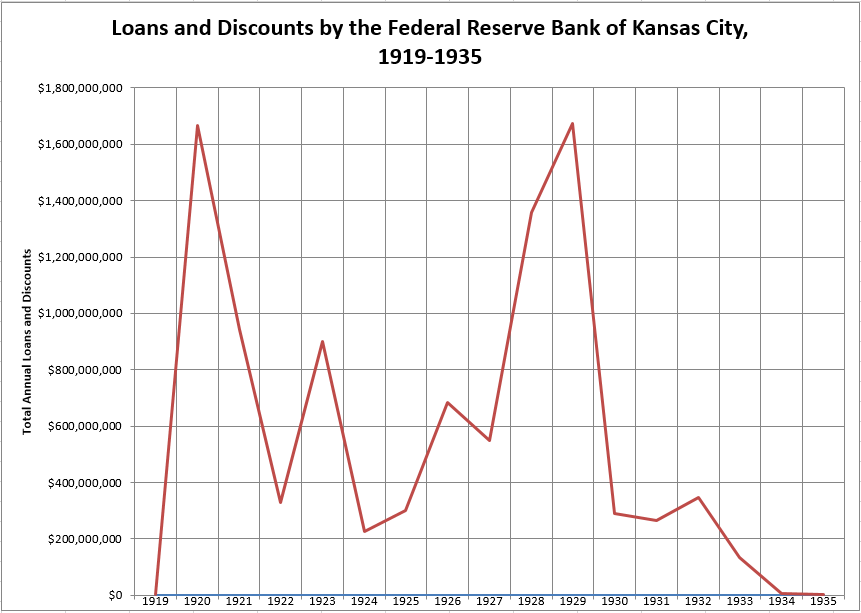

The following figure illustrates the instability of the regional economy during the interwar years. The steep decline in lending between 1920 and 1922 indicated the post-war agricultural crisis and the constriction of credit following the Fed’s raising of interest rates. Another decline in 1924 reflected “heavy liquidations of indebtedness to banks and increased deposits” among member banks. While this period suggested improvement in the fortunes of member banks, it came at the expense of borrowers whose loans had been terminated or foreclosed. Depressed levels of borrowing from the Federal Reserve indicated less overall growth across the regional economy.

Periods of higher demand for loan discounts, on the other hand, marked years of stronger economic activity. In the late 1920s, prices for farm commodities rose and production on farms and in manufacturing centers was high, while the construction industry, wholesale, and retail trade expanded. These positive indicators resulted in better banking conditions, including higher deposit levels and larger balances with the Federal Reserve.

But banks in the region did not increase their loans to regional producers, despite improved circumstances. Bankers in the region continued to demand loan repayment rather than extend the terms of the loans. Borrowing from the Federal Reserve Bank continued to support member banks’ investments in stocks and other financial instruments, rather than local lending. The Fed reported that banks’ Wall Street investments drove up the interest rates for local credit, and in 1929 suggested that the strong investment opportunities in the first three-quarters of the year (before the stock market crashed in October) meant that “banks were having difficulty in caring for all the credit needs of their communities.” Once again the Federal Reserve did little to restrain member banks from their troublesome investment practices.

The central bank research team and academic economists remained fearful that runaway stock prices constituted destructive speculation. Yet efforts to contract the expansion of credit and thus curtail this speculation in the late 1920s failed, as evidenced by the crash of October 1929. The Federal Reserve proved equally unable to stimulate credit in the coming years.

Reports from the central bank between 1930 and 1935 speak to the bottoming out of the lending business during the Great Depression, as represented by the figure above. The Federal Reserve purchased fewer loans from member banks; such activity declined 83 percent between 1929 and 1930. In 1935, the Federal Reserve’s lending volume reached only 0.2 percent of the total for 1929. The Federal Reserve rejected some loan purchase requests from member banks, judging them ineligible or lacking in collateral. The institution failed to embrace its role as “lender of last resort,” which would have meant refinancing loans backed by poor securities. Manipulation of interest rates did little to produce a recovery when the Fed proved unwilling to follow through by purchasing bank loans.

The Federal Reserve's inability to control the regional and national economy was magnified in the large number of failed banks throughout the region in these years. Many of these failures occurred in the countryside, resulting from local banks’ inability to collect on farm mortgages and livestock loans. Some of the banks that went out of business were Federal Reserve members, which suggested that the system could not prevent major losses, as its founders had hoped.

Still, a greater proportion of the failed banks were small, non-member state banks. The Federal Reserve Bank of Kansas City attributed such closures to these banks’ lack of capital and reserves, or inability to afford good management. Failed banks often had been unable or unwilling to meet the standards of the central bank, such as its reserve and capitalization requirements and demands for federal auditing. State banks operated with much smaller capitalization than national banks (only $5,000 in a town of 3,000, compared to $25,000 for national banks in similarly sized towns) and had greater freedom in lending on farm real estate. State bankers were reluctant to cede their independence by joining the Federal Reserve, and Fed officers viewed the high bank failure rate as the result of banks’ refusal to become members of the system.

In its 1927 annual report, the Reserve Bank called the trend of bank failure “the process of elimination of weak or unprofitable banks.” As a result of closures and mergers, around 900 fewer banks operated in the district compared to 1920. The number of member banks in the region continued to fall, from 3,593 in 1928 to 2,430 in 1932. Banks in Kansas City were not immune from these troubles; the city witnessed 33 bank failures between 1920 and 1928, though some reorganized or consolidated. The decade started with 55 banks operating in Kansas City, and only 40 existed by 1928.

During the following years, forces other than Federal Reserve policy stimulated any gains in economic activity seen in Kansas City and the surrounding region. A large part of the city’s growth during these years fulfilled the aims of the Ten-Year Plan, a $50 million, bipartisan bond project approved by Kansas City voters in 1931 to counter the effects of the Great Depression by financing infrastructural improvements and the construction of a new city hall, county courthouse, and municipal auditorium. Tom Pendergast’s Ready Mixed Concrete Co., along with the machine boss’s coordination of pick-and-shovel work for thousands of unemployed laborers, provided much of the momentum for these projects even before the New Deal used federal authority and funds for similar relief programs. Two other major developments, the Nelson-Atkins Museum and the University of Kansas City, opened in 1933 after decades of planning.

Under the impetus of these projects, Kansas City and other urban areas in District Ten did begin to see signs of relief by the middle of the 1930s. Retail and wholesale trade increased by double digits, while construction also witnessed healthy gains. Some urban production industries improved, including flour and cement processing, and regional production of zinc, lead, coal, and petroleum rose.

Although the business community furnished leadership in the establishment of the Ten-Year Plan, these projects did not owe to any strong financial incentive among the city banks. Wealthy donors who co-sponsored some of the projects, the political machine, and the voters offered the vision and the willpower to keep Kansas City moving forward even during the depths of the Great Depression. As a relief effort, the projects at least made it appear that the city was coping with the economic turmoil better than many other cities.

The recovery efforts of in the city did not extend to the farms of the Federal Reserve district. Farmers suffered through the worst drought in memory, and amid the Dust Bowl produced the smallest harvests on record. Here, too, forces besides the Federal Reserve would drive economic activity. The federal government’s New Deal allotment contracts for reducing planted acreage or breeding in several key commodities provided much needed subsidies to farm incomes, some $127,490,000 throughout the District in 1934. The federal government also purchased $170,297,000 worth of livestock, seed, and other farm commodities, and then channeled them into urban processing centers.

Benefit payments from New Deal programming began to intervene in supporting crop prices and providing a small measure of stability to the agricultural economy, including Kansas City’s processing industries. Government accounts meant that flour and meat production recovered in 1934. Some of these trends continued through 1935. New Deal programs, rather than renewed bank investment, deserve the credit for propping up the District’s interwoven rural and urban economies. As illustrated in the figure above, interbank lending within the Federal Reserve System remained close to zero throughout the early 1930s.

Despite a vision of its own strength, the Federal Reserve Bank did not play a particularly strong role in shaping the regional economy during the 1920s and 1930s. It promoted principles of conservative banking by encouraging banks to terminate questionable loans, but did little to encourage lending to viable producers who needed it. The bank also failed to push banks in the district away from investing in stocks and city call markets and toward intraregional lending to farmers and industrialists.

The Federal Reserve was not yet a major national economic policymaker, and the system would require Congressional strengthening during the New Deal to achieve its mostly uncontested status as the arbiter of the national financial system. The Banking Acts of 1933 and 1935 introduced the Federal Deposit Insurance Company and stipulated that banks with deposits of more than $1 million that wished to be members of the FDIC had to join the Federal Reserve by July 1942. These laws finally gave many banks a powerful incentive to join the central banking system. With greater control over more of the national banking structure, the Federal Reserve would become its chief regulating force and an important source of public confidence. Kansas City, too, would finally take its place as the heartland’s financial center during the post-war years.

A longer version of this article is published in the book, Wide-Open Town: Kansas City in the Pendergast Era (University Press of Kansas, 2018), edited by Diane Mutti Burke, Jason Roe, and John Herron.

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.